Market Updates

2nd of July 2020

Market Updates for JuLY 2020

|

Dow Jones 30 |

S&P 500 |

Nasdaq |

FTSE 100 |

Euro Stoxx 50 |

Nikkei 225 |

|

1.33% |

1.46% |

5.30% |

0.05% |

4.15% |

1.02% |

|

US 10YR |

Brent Crude |

Gold |

GBP:USD |

EUR:USD |

USD:CNY |

|

0.63% |

$41.14 |

$1,781 |

1.24 |

1.123 |

7.065 |

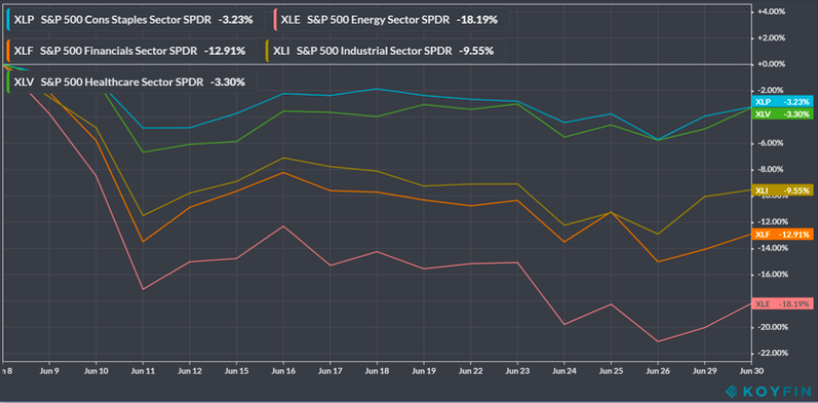

The risk-on sentiment experienced in May continued into the beginning of June, with equities performing strongly until June 8th. This was followed by a period of risk-off sentiment rolling into month end. The sector rotation (demonstrated via US sectors) was prodigious, with cyclically orientated sectors such as energy, industrials and financials providing double digit positive returns, but subsequently this short term trend reversed. The below highlights the extent of this rotation from June 8th, with industrials, financials and energy reversing 10%, 13% and 18% , respectively, and lagging defensive sectors, such as consumer staples and healthcare which fell 3.2% and 3.3%.

Chart Source: Koyfin Charts

Almost 50% of the US population are currently experiencing unemployment according to the National Bureau of Labour statistics, compared to 41% at the peak of the GFC. Unemployment will continue to suffer in the short term due to 40% of US states re-imposing certain lockdown

measures ahead of the 4th July weekend, with social spaces including beaches, bars, cinemas and gyms being forced to close. Generally leading economic data, as represented by IHS Markit Flash data, beat consensus estimates and returned to levels last seen in February and March. Although one should remain cautious on the economic front, industrial output and new orders continue to decrease, albeit at a slower pace throughout June.

Record global debt issuance continued in June as governments desperately attempt to dampen the impact of Covid-19. For instance, the UK raised £225bn in the first half of 2020, double the amount raised during the full year in 2019. For the first time since 1963, the UK’s debt to GDP ratio rose above 100%. Increased leverage among public balance sheets will continue unabated, particularly within the developed world, especially in the EU, as the bloc’s fiscal response to Covid-19 is still to be finalized. In response, government bond yields rose markedly in early June. Notably the US 10 Year peaked at 0.90%, however risk-off sentiment consequently triggered a ‘flight to safety’ with the US 10 Year closing at 0.63%.

News flow surrounding Covid-19 deteriorated relentlessly in June, with Brazil materializing as the current epicentre. Jair Bolsonaro’s uncoordinated and lackadaisical approach to combating Covid-19 has attracted global attention, after the country experienced its worst week of new Covid-19 cases (250,000) and second highest weekly death toll (7000). Staying in LATAM, Argentina also extended lockdown measures, relating to the greater Buenos Aires area, for a further 2 weeks, having been one of the early movers in responding to Covid-19 with primary lockdown measures implemented in March. Seemingly Brazil is not an isolated scenario, with India also experiencing their highest amount of new cases in recent weeks (circa 20,000 per week). China has also re-imposed lockdown measures in Anxin Province near Beijing, which initially will affect 400,000 people. Encouragingly European governments are showing signs of confidence, with gradual reopening’s occurring throughout and ‘air bridges’ being implemented to allow more flexible travel within the region.

Gold closed at $1781 returning 3.5% in June, and continues to threaten the next level of technical resistance between $1780-1800. A weekly close above this level could signal a price surge which challenges gold’s all time high of $1921. Brent Crude had another positive month, up 17.5% and closing at $41, pushing to challenge the March 5th resistance line of $45. Similarly to equities, Brent lost ground after June 8th with concerns arising regarding further demand destruction caused by a 2nd wave of Covid-19. OPEC+ committed to continuing their 10m barrels per day cuts until 31st July. The current cooperation between Russia and Saudi Arabia means the agreement remains intact, with both parties shouldering the majority of the cuts.

The democrat held House of Representatives passed a stimulus act named the Heroes Act in May, and unsurprisingly the republican held senate referred to the act as ‘dead in the water.’ Thus a reincarnation of the CARES Act, which is currently being applied, is the most likely form of fiscal stimulus approaching. Markets will be monitoring such developments closely, as by the end of July credit card/auto loan forbearance and enhanced unemployment benefits will have ended, various local and state budget cuts will have begun and tax receipts are due on 15th July. This combined fiscal and credit easing is being withdrawn just as markets are seeking evidence of stimulus to ‘fuel’ a recovery. Early US presidential election polls indicate Joe Biden as favourite with up to a 25 point lead. Heading into the election it remains of use to recall that President Trump trailed throughout the whole presidential campaign in 2016. Interestingly, of the last 110 polls taken prior to the 2016 election only 10 polls showed a Trump victory. One

should expect such polling inconsistencies to continue. Policy implications to reflect on include whether financial markets would prefer a Biden or Trump win. Given the socialistic biases present in candidates such as Bernie Sanders, it seems the Democratic Party as a whole has become more left leaning. Such an outcome will become clearer once each candidate releases their policies. If such a scenario materializes, objectively, a Trump victory may well be deemed more favourable from a financial markets perspective.

Western markets can often be uneventful during the summer months, and investors will be increasingly focused on whether further fiscal stimulus, among other policies, is introduced. The FED began to contract their balance sheet in late June, which will be another interesting test for markets, particularly the extent that they can function without the FED’s interventions.

Passive Investing: The Carthaginian stalemate or the Barbarian Hordes

The debate between active and passive investing seems to be everlasting. Passive has become increasingly influential in money flow terms over the last decade, albeit in an increasingly low volatility environment. The selloff in February and March was the first period of serious pressure the modern wave of passive investors has needed to withstand. Will this period be a mere blip on the radar, similar to Hannibal and his Carthaginian Army’s 15 year campaign on mainland Italy against an emerging Rome, which ultimately marked the rise of Rome and the fall of Carthage (Rome, led by Scipio, eventually counter attacked the Carthaginians and conquered Carthage). Or will this represent the sacking of Rome by the Barbarian Hordes in 411, which in hindsight represents a significant turning point of the fall of Rome, and sets the scene for the dark ages of Europe. The data seems to imply the former is most probable, with no signs that the influence of passive investing will peak any time soon.

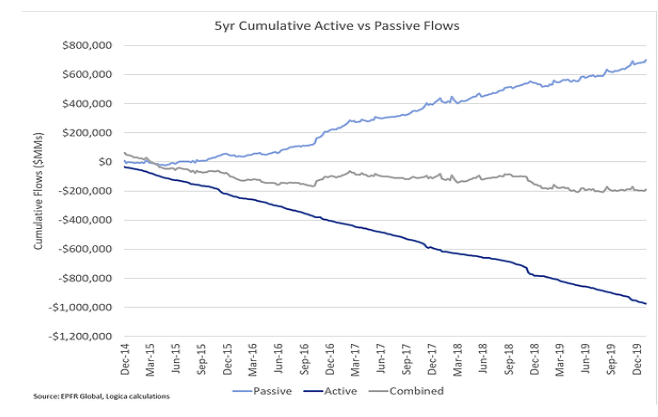

The majority of passive vehicles (namely ETFs and OEICs) are efficient ways for a macro aware investor to express their views, and are an asset when managing client portfolios. ETFs incorporating thinly traded credit and emerging markets can, however, produce extra risks than what investors expect during sharp sell offs. For instance, even large US based investment grade bond ETFs traded at 7% discounts in March (ETF discounts/premiums should be marginal), reminding investors that ETF’s will (eventually) only be as liquid as the underling holdings. One would assume such an area is ideally suited to active management. Passive flows are of such magnitude that surely at this point active managers must consider passive flows when making decisions within an active strategy, especially assuming these passive flows will contribute to returns, despite being insensitive to valuations. Markets represent the activity of buyers and sellers, rather than information. Thus pure valuation based investment frameworks (which can be profitable during certain environments) naturally swim against the tide during continual periods of valuation insensitive money flows. This is representative of not just the last 3 months, but the last 5 years. Eventually passive investing may represent the transmission function by which the majority of investing occurs. Currently 100% of gross fund flows into stock markets are passive, with the corresponding redemptions experienced by active managers shown in below graph. Circa 60% of 401k plans holda vanguard (passive) target date retirement fund. One can simply extrapolate this divergence forwards for an idea about possible future flows, and the knock on effects for active investing.

Chart Source: Logica Investments

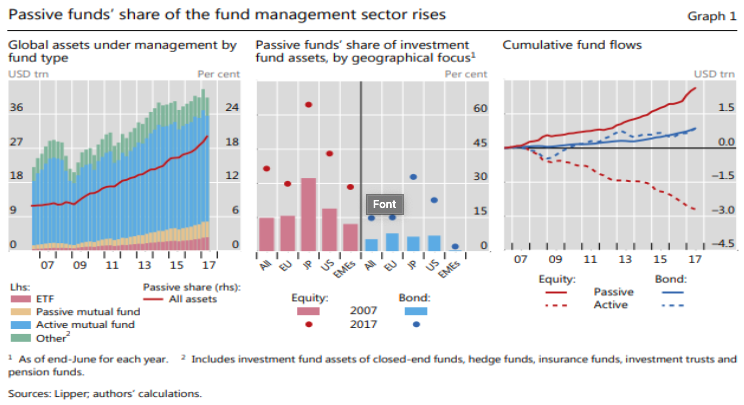

The market share of US equity funds (a $9 trillion market) represented by those which are based on passive indices has grown to over 50%, beating active equity funds for the first time in 2019. This number has doubled in the last 10 years. Although this only represents 12% of the total US equity market. Global markets could look substantially different in future years if this trend continues. The trend is visually highlighted below via an extract from a 2018 BIS report.

Chart Source: BIS

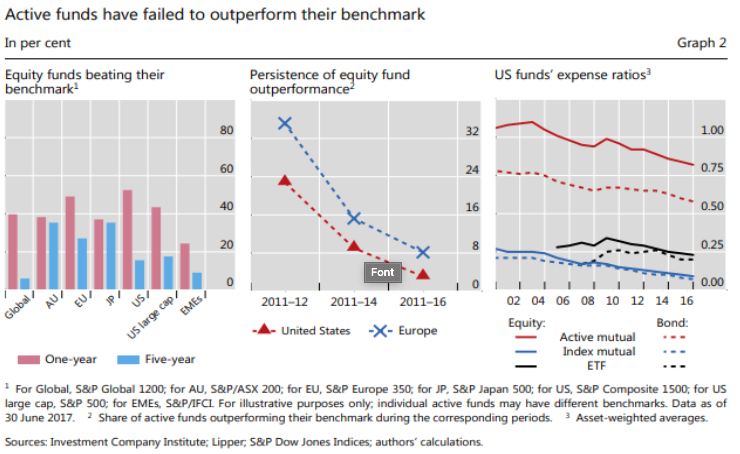

As the below graph evidences, active managers have struggled to outperform (after fees) their benchmarks over a period such as 5-years, representative of a realistic investment time frame. Correlation obviously does not always mean causation, but it is intuitively difficult to ignore such trends in active management. Regulatory changes may also play a role, with increased scrutiny on ‘value for money’ when providing investment advice.

Chart Source: BIS

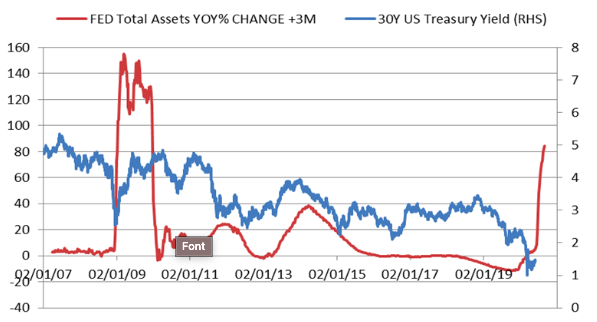

The trend towards passive investing has been relentless, but is now the ideal time for active management when considering the macro environment? Especially as factors that need to be contemplated, such as severe central bank policy changes & global debt levels, are much more extreme today than 10-15 years ago. The below graph, which was referred to last month, shows the potential for a significant rise in government bond yields. This is a tail risk that markets may not have fully factored in, with plenty of historic evidence to support.

Chart Source: St. Louis Fed

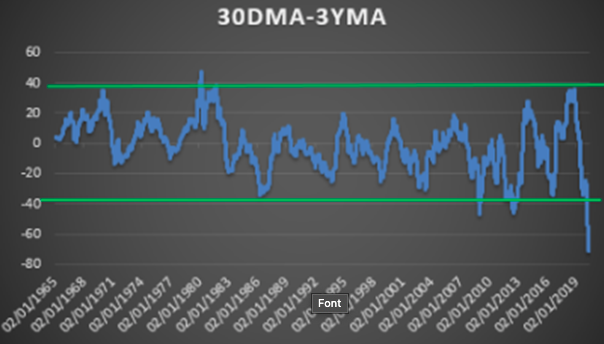

The next graph represents the structural momentum of the US 10 Year treasury market, which is useful when normailizing market activity compared to historical levels (and also identiying trends). The current data point of circa -70 is excessively bullish (lower yields), to an extent not seen in 50 years. Again hinting at the possibility of a longer term rise in yields. One questions the extent that markets could handle such a setup, and the popular conclusion is that a form of modern monetary theory will be implemented through yield curve control. Such policies were last used in the 1940’s to surpress the governments war time borrowing costs. Given the ‘unknowns’ present one would be hard pressed to ‘sell’ a passive over active strategy during such a period.

Chart Source: St. Louis Fed

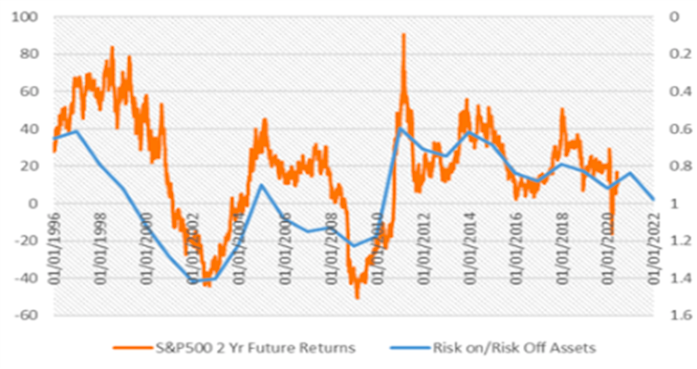

Lastly, it is imporant to consider the mix of risk-on versus risk-off assets, which can enable one to project a possible future trajectory for S&P 500 2 year forward returns. For this purpose, risk-on assets are represented by the market capitalization of US equities, and risk-off assets the total value of US federal debt outstanding and M2. The interplay between both asset types is slow moving, but once one asset gains noticeable dominace over another returns are often skewed in one direction. Two periods which stand out are the year 1999- 2000 and 2007-08, where risk-on assets started to outweigh risk-off assets, which implied two year forward returns between-20 & -40%. Comparing this to 2020, the outlook for 2 year forward returns is less dire, although the two year data lead suggest circa 0% should be expected. This is caveated by the fact that no prediction of short term returns is made, thus one can not rule out all time highs being reached before the two year return stream is completed.

Chart Source: Koyfin Charts, St. Louis Fed

Despite the data suggesting passive flows will continue to dominate at the expense of active management, the macro fundamentals suggest one should operate cautiously if relying on passives. The concluding remark is that within the market structure of the fixed income and equity space is one which hasn’t been experienced (or considered) for a decade. Such an environment typically includes higher volatility and more unknown ‘unknowns’. The end result in terms of equity or fixed income prices may be similar, but history suggests that the journey to achieve such ends may be volatile, and such an environment will pay to operate an investment strategy with an active bias.

Download this Market Update

Disclaimer

This report was produced by Global Preservation Strategies (“GPS”). The information contained in this report is for informational purposes only and should not be construed as a solicitation or offer, or recommendation to acquire or dispose of any investment. While GPS uses reasonable efforts to obtain information from sources which it believes to be reliable, GPS makes no representation that the information or opinions contained in this report are accurate, reliable or complete. The information and opinions contained in this report are provided by GPS for clients only and are subject to change without notice. You must in any event conduct your own due diligence and investigations rather than relying on any of the information in this report. All figures shown are bid to bid, with income reinvested. As model returns are calculated using the oldest possible share class, based on a monthly rebalancing frequency and all income being reinvested, real portfolio performance may vary from model performance. Portfolio performance histories incorporate longest share class histories but are either removed or substituted to ensure the integrity of the performance profile is met.

The information contained within this website is subject to the UK regulatory regime and is therefore primarily targeted at customers in the UK. The information contained within the websites does not constitute investment advice or a personal recommendation for any product and you should not make any investment decisions on the basis of it. The value of investments and the income from them can fluctuate and it is possible that investors may not get back the amount they invested.

Global Preservation Strategies Limited is registered in England and Wales No 07354963 and authorised and regulated by the Financial Conduct Authority (No. 568328). GPS Wealth is a trading name of Global Preservation Strategies Limited.